Integration as a Key Enabler of Financial Crime Prevention

| | Senior Vice President Strategic Product Management and Analyst Relations

The last five years have seen rapid growth in the number and variety of available payment systems, alongside an explosion of public adoption in the wake of the COVID-19 pandemic. But this change of technological pace has also led to significant increases in financial fraud, with scams becoming ever more sophisticated and difficult to detect. According to a 2022 survey by accounting firm PwC, 44% of those polled in the financial services industry reported experiencing customer fraud in the previous 24 months, 38% cybercrime and 29% know-your-customer failure. The cost for cybercrime prevention grows accordingly, with a large part of that in labor costs. Classic hands-on approaches to FRAML (fraud and AML) prevention are increasingly incapable of keeping up with rising fraud alarms, false positives and the high number of associated manual tasks. This blog highlights innovations in the financial crimes compliance field that can help institutions balance risk identification and loss prevention against faster transaction processing – in turn leading to increased customer satisfaction.

Key challenges in fraud prevention and AML

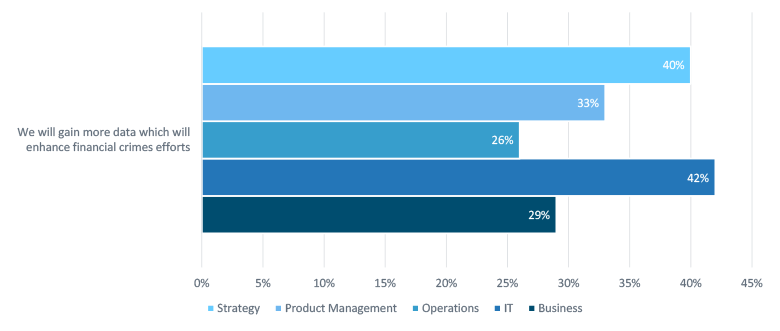

The fight against fraud and AML is not new, but rapid technological progress and the changing fraud landscape are forcing financial institutions to adapt at an unprecedented rate – across their entire ecosystem. The joint Q4 2022 global survey on ISO 20022 readiness by SEEBURGER and Celent found that gaining more data that will enhance financial crimes efforts was cited as one of the main benefits expected from ISO 20022 across all roles and responsibilities.

Source: Celent Global ISO 20022 Readiness Survey, 2022.

Some of the typical challenges are:

Outdated and inefficient systems: Old and inefficient systems often operate on a strict if-then logic. Their inherent lack of nuance generates a large number of false positives, which in turn can degrade effectiveness and thereby increase the operational risk. This creates a lot of “noise” the institutions’ staff then has to deal with on a one-on-one basis, which can delay customer transaction request processing and thereby customer satisfaction.

Complex data sources and manual processes: Internal data is often unstructured, fragmented and incomplete. Residing in multiple disparate and unconnected systems, this messy data can drive up costs and consume significant resources. Operations are heavily reliant on people in order to gather, consolidate and analyze data, which in turn can lead to overworked staff and poor decision-making – heightening the risk for financial fraud. It can be difficult to keep ahead of the results and alerts of multiple systems. By integrating all financial crime alerts into a single customer view, data can be converged in an easily accessible format

Back-office ops for the front office: Cutting-edge technology can only be as good as the people who work with it. In order to profit from innovative technology and use it to improve resilience, the people using the system must understand how it works – and what it’s capable of. Many people still think of analytics as something that is used only in back offices, and it does have its place there. But if it’s supposed to live up to its full potential in FRAML (fraud and AML) prevention and successfully curb risk, analytics needs to be incorporated in the front office as well.

Cloud: After a long period of careful hesitation out of initial security concerns, financial institutions are increasingly moving their applications into a cloud-managed service environment to better keep pace with the rapidly changing technology. It’s only a matter of time before they also start moving their FRAML operations into the cloud, be it on a short-term tactical or long-term strategic basis.

Escalating financial crime threats in a constantly evolving regulatory landscape call for a proactive and more risk-based approach to fraud prevention, detection and compliance. Particularly for smaller regulated institutions without large analyst and investigative teams, the challenge will be to make the necessary analytics tools accessible for a business user or in a citizen integrator approach.

Advances in FRAML technologies

In order to overcome these challenges and effectively process FRAML-relevant data into useful information, typically, an intelligent, agile and scalable platform is needed. New, AI-based advancements in computing abilities, analytics and cloud-based technologies can help to drive operational efficiency and reduce total cost of ownership, while at the same time improving the customer experience. The following are just a few examples from a wide variety of new approaches.

Machine learning (ML)

Rules-based systems have been the state-of-the-art in FRAML for over 20 years for a reason, but whether an activity is suspicious or not is very subjective and depends on the judgment of the person working with the system. By contrast, supervised machine learning leverages a variety of algorithms based on, among other things, statistical analysis and probabilities. Using a training set of data and valid outputs, models can “learn” to detect patterns at a level that would be almost impossible for humans to detect, and make predictions and recommendations accordingly. Unsupervised machine learning is allowed to explore data without knowing what the desired output should be and instead identifies patterns and clusters in the data for further analysis.

Robotic process automation (RPA)

Robotic process automation is primarily used to automate internal and external data collection, process transactions and subsequently identify risks much faster than a manual process, which helps free up valuable personnel for more important operations. Using RPA in combination with an integration platform is an ideal approach, where data can be securely enabled through different types of integration capabilities, such as B2B/EDI, MFT and API.

Natural language processing (NLP)

NLP technology can be thought of as a funnel that catches the unstructured data, structures it and channels it further downstream where it can then be used for detection and investigation purposes. This way it is able to provide valuable context to facilitate and improve fraud detection. It can be set up to flag specific activities, which the investigative team can then dismiss or review.

Artificial intelligence is able to work at an in-depth level that is unsustainable for human investigators and can uncover hidden relationships, detect subtle behavioral patterns and extrapolate predictions for future risks. By automating these processes at scale, it enables fraud and AML analysts to identify potentially fraudulent transactions through complex money monitoring. Better data intelligence yields faster, higher-quality and more consistent results as a basis for decision-making and helps to utilize the skills of the investigative team to their fullest potential. Institutions should leverage these advanced technologies for all work that doesn’t need human intervention wherever possible.

Think about your data ecosystem!

Data is the lifeblood of the financial ecosystem. It flows in from a plethora of sources, including customer profiles, transactions, business processes, customer service experiences and even external sources, such as third-party vendors; and it’s stored in a variety of different formats. In order to become the foundation of successful operations, this data must be collected, organized, stored and analyzed before it can be transformed and channeled accordingly. This data can be used to identify risk factors such as fraudulent activities or money laundering – but only if it is made available in the appropriate form. The inability to access and harness the frequently incomplete or fragmented data for effective financial crime risk detection and analysis is often at the root of continuing fraud and AML deficiencies.

ISO 20022 will introduce standardization, structure and richer data across the global payments landscape. Indeed, 37% of North American banks polled in the 4Q 2022 global survey on ISO 20022 readiness by SEEBURGER and Celent cited FRAML as one of the key benefits they expect to gain from the migration.

Source: Celent Global ISO 20022 Readiness Survey, 2022.

By implementing and using ISO 20022 enabled by an agile, secure and scalable integration platform, banks will be able to manage risks with more granular monitoring options:

Transaction monitoring:

- Capitalizing on additional remittance data, including structured information on debtors and creditors.

- Access to more detailed payment fields to improve the identification of patterns, such as specific combinations of risk characteristics within transactions that are associated with criminal activity.

- Improving teams’ understanding of end-to-end payment flows and counterparty verification, resulting in more robust risk coverage.

Fraud monitoring:

- Improving the identification of fraudulent payments and enabling more efficient fund recovery through higher quality data.

- Enabling real-time monitoring and tackling of more complex fraud risk.

- Improving existing fraud monitoring controls, identifying pain points, and overlaying transactions with additional and higher quality data.

By establishing an intelligent, predictive fraud prevention and AML program, and using an agile, secure and scalable integration platform, financial institutions can not only advance financial crime prevention, detection and investigation, but also make them smarter and faster. A holistic risk profile of customers, accounts and transactions yields better intelligence that allows the investigative staff to focus on the real problem cases instead of wasting time on background chatter. This simplified IT infrastructure, lower costs and a more holistic risk management help to increase revenue and foster customer retention.

How SEEBURGER helps

At SEEBURGER, we have worked with some of the world’s top banks for many years and gained deep insight into the inner workings of their core systems and applications. This has given us an intimate understanding of what their business needs are, how data has to be integrated and managed and what challenges banks face when migrating to new infrastructure and creating new services. With this knowledge, we are uniquely positioned to help make your transition as smooth and successful as possible.

With the SEEBURGER Payments Integration Hub, you can address the onboarding of corporate customers and their data transfers, self-services for testing and configuration, application integration, validation and transformation aspects (including conversion to the new messaging standard ISO 20022) of the payments integration process – fast, friction-free and agilely scalable at need.

Whitepaper

Download the full report on the survey “Ready Or Not – Here It Comes: There’s No Hiding from ISO 20022” here:

DownloadThank you for your message

We appreciate your interest in SEEBURGER

Get in contact with us:

Please enter details about your project in the message section so we can direct your inquiry to the right consultant.

Written by: Ulf Persson

As SVP Strategic Product Management and Analyst Relations, Ulf is responsible for strategic product management, product marketing, global analyst relations and leadership with regards to SEEBURGER integration technology, platform and integration services. This also includes strategic sales and marketing initiatives. Ulf works across multiple industry verticals such as Financial Services/Payments, Automotive, Logistics, Utilities, Retail, CPG and Manufacturing. Ulf has more than 30 years of global business and technology experience working with product and solution delivery of integration technologies (EAI, EDI, B2B, MFT, API, etc.), Analytics and Big Data, Cloud Services, Digital Transformation and various industry initiatives. Before joining SEEBURGER in October 2016, Ulf worked in various global leadership roles with international business integration technology and cloud services providers.