ISO 20022: The Corporate Journey Starts Now

| | Senior Vice President Strategic Product Management and Analyst Relations

The messaging format ISO 20022 is poised to become the global payments standard of the future. While Swift’s projected migration deadline of November 2025 only applies to banks for now, this does not mean that corporates are unaffected by the migration. For a time at least, banks will continue to support other formats for their corporate customers, but as the new standard gains traction, they will likely start levying fees for this service. Since a large number of corporates are multi-banked, these fees may quickly add up. And once Swift judges that the migration is complete, they will retire the older MT messaging format altogether, meaning that corporates who have not made the switch at that point will not be able to do business, period. In this article, we look at what ISO 20022 means for corporates and why the migration may not be as optional for them as they think.

In our interview, SEEBURGER expert Ulf Persson, Senior Vice President Analyst Relations, explains the basics and answers the most pressing questions around ISO 20022.

![]() ISO 20022 – 20 Minutes, Endless Answers

ISO 20022 – 20 Minutes, Endless Answers

SEEBURGER Podcast by Ulf Persson & Jennifer Monz | 13 July 2023

Why do corporates need ISO 20022 at all?

As a payments format, ISO 20022 is not new. Particularly in Europe, it has been widely used ever since the Single Euro Payments Area (SEPA) introduction. But even now, corporates often use outdated format versions, meaning clearing systems and other players are unable to take full advantage of the richer data contained in ISO 20022 messages. Instead, the data is truncated and partly lost before it ever reaches the addressee. And financial institutions will, each at their own pace, gradually stop supporting the old MT formats for their corporate clients. Swift explicitly cautions corporates on its website: “As of 2025, banks might require their corporates to be fully ISO 20022 compliant.”

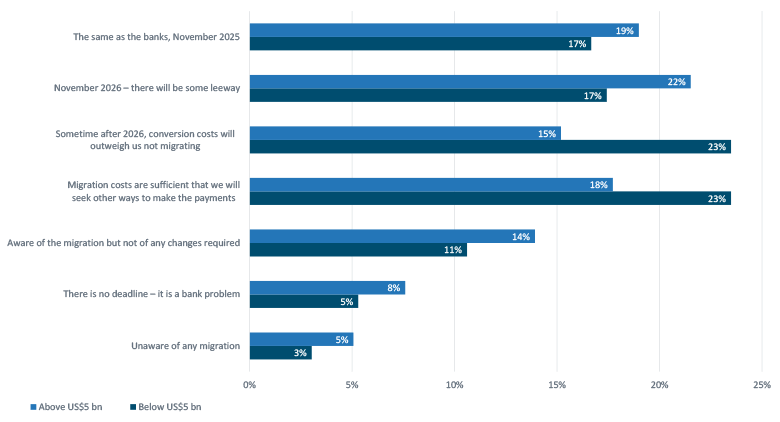

In the joint Q4 2022 survey “Ready Or Not, Here It Comes: There’s No Hiding From ISO 20022”, SEEBURGER and leading research and advisory firm Celent looked at where the industry stands in terms of their journey towards ISO 20022 readiness. Globally, just 18% of corporates polled were working towards the November 2025 deadline – with a staggering 42% of global corporates making no plans for the migration at all or looking at alternate solutions.

Source: Celent Global ISO 20022 Readiness Survey, 2022

Yet as of the time of writing this blog, some banks have already started requesting from their financial service and system providers that data be formatted into the new format. However, since there is no official regulation concerning this, each bank may decide how to handle the situation individually: some may choose to extend the timeline for their corporate clients; others may not. Being fully ISO 20022 capable would erase this problem for corporates altogether.

Key ISO 20022 challenges for corporates

Corporates are at different levels of maturity on their ISO 20022 journey. That means there is no one-size-fits-all approach. Working with an ISO 20022-native vendor – either their existing one or a new one – can help corporates evaluate where they are in their ISO 20022 journey, what they still need to do and how to best address individual pain points.

The change to ISO 20022 will have a significant impact on how company systems send and receive payment information from their banks. ERPs, TMSs, HR/payroll systems, solutions built in-house and all the systems feeding payment information into them will be affected. This will require internal system enhancements regarding what data is needed and where it is stored, resulting in significant cost in terms of IT time.

Corporates who don’t take action now risk receiving incomplete information if they continue using MT940 or MT942 for their banking information. These older formats are unstructured with limited fields. If the payment originator uses ISO 20022 XML format, the incoming data may be truncated if the receiver is still using MT. This will make reconciliation difficult and prone to errors.

ISO 20022 benefits for corporates

Of course, it’s not all dire. Swift would not introduce a new standard if it didn’t have significant benefits for the industry. Nor is it just the banks who profit, while corporates have to tag along. The benefits accrue for corporates as well:

Standardization: Businesses are constantly striving to standardize processes across their organization and across regional branches. Currently, the lack of interoperability between legacy and new payment infrastructure makes the standardization of data difficult. ISO 20022 standardization helps to drive efficiencies through reduced data truncation and improves the cross-border payment experience.

Cost Reduction: ISO 20022 sets out to simplify the fragmented and complex global payments landscape. Its highly structured, rich data allows for the end-to-end automation of previously labor-intensive manual processes – including local languages and scripts.

Productivity: The richer data and remittance information contained in ISO 20022 allow for improved auto reconciliation and improved posting rates for accounts payable and accounts receivables teams. This increased efficiency and productivity can in turn boost payment processing. Another benefit is heightened visibility of cash flow and liquidity, enabling decision-making and strategic planning.

Risk & Compliance: Faced with an ever-faster evolving fraud landscape, global risk management is always a top priority for financial institutions. As a global payment messaging standard, ISO 20022 allows banks to ensure compliance with frequently changing regulatory reporting requirements. Risk and compliance teams benefit from highly structured data, allowing higher payment transparency, as well as insight into payments on behalf of third parties (POBO).

Customer Experience: Cross-border payments have been a pain point for both banks and their customers for years. In ISO 20022, payments contain the corresponding remittance details, meaning account reconciliation can be automated. The standardized message semantics and syntax facilitate transmitting global transaction information.

The transition to ISO 20022 will be a significant factor for corporates in terms of cost, time and resources – but done right, the benefits far outweigh the challenges. Corporates who embrace the transition now and look to future-proof as much as possible stand to gain significant value from the payments they process. On the flipside, corporates who now seek to do only the bare minimum may find themselves unable to reap the full benefits ISO 20022 has to offer down the line.

So what should corporates do to become ISO 20022-ready?

Becoming ISO 20022-ready is not just an IT-conversion project. Processes must be reviewed, changed or updated and mapped. But the change has to begin with the mindset of the people working with them. It is not enough to merely train them in new technology. As long as they don’t grasp the importance of the change, they won’t be able to understand, strategize and identify the business benefits. If they don’t see the benefits, they won’t put in the effort, and if they don’t put in the effort, it won’t matter how good the technology is. Knowledge and education are key.

Eventually, all stakeholders in the payments process will have to eliminate outdated formats and adopt ISO 20022 or partner with a vendor who can support a seamless translation for any type of format into an ISO XML standard message. On-premise systems that cannot be changed easily or cost-effectively will become an issue. Partnering with a competent vendor can help to configure older ERP-systems to improve straight-through processing and support rich and structured data for compliance and due diligence.

How SEEBURGER helps

The SEEBURGER Payments Integration Hub is a secure and scalable single platform with modular and agilely configurable components that allow you to be ISO 20022-ready rapidly and at a low cost. It handles data conversions, compliance and back office integration, leading to better automatic reconciliation and accounts payable and receivable automation, as well as faster straight-through-processing. Ready-made application connectors map and translate different payments formats to ISO 20022 without disruptions to your workflow, systems and applications. This will enable better cash management and visibility.

Our best-of-breed technology helps you meet regulatory reporting requirements with ease while staying ahead of fraud and cybercrime prevention with fully structured payor input, including POBO (payments on behalf of) beneficiaries.

Whitepaper

Download a summary of the key highlights for corporates from the SEEBURGER and Celent report here:

DownloadThank you for your message

We appreciate your interest in SEEBURGER

Get in contact with us:

Please enter details about your project in the message section so we can direct your inquiry to the right consultant.

Written by: Ulf Persson

As SVP Strategic Product Management and Analyst Relations, Ulf is responsible for strategic product management, product marketing, global analyst relations and leadership with regards to SEEBURGER integration technology, platform and integration services. This also includes strategic sales and marketing initiatives. Ulf works across multiple industry verticals such as Financial Services/Payments, Automotive, Logistics, Utilities, Retail, CPG and Manufacturing. Ulf has more than 30 years of global business and technology experience working with product and solution delivery of integration technologies (EAI, EDI, B2B, MFT, API, etc.), Analytics and Big Data, Cloud Services, Digital Transformation and various industry initiatives. Before joining SEEBURGER in October 2016, Ulf worked in various global leadership roles with international business integration technology and cloud services providers.