REFIT – a Refurbishment for EMIR

| | Senior Consultant - Business Unit Utilities, econtea GmbH

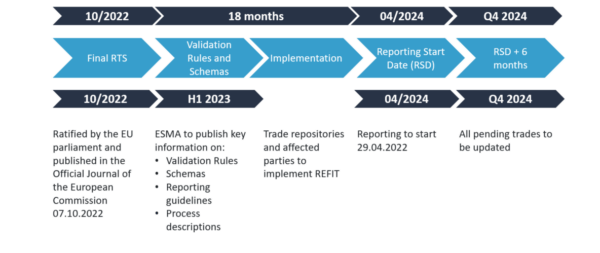

+++ Update 07.11.2022: REFIT – The fitness programme for EMIR: the timetable is fixed

The European Commission has published the Regulatory Technical Standards (RTS) and the Implementing Technical Standards (ITS) in the Official Journal of the European Union of 07.10.2022.

EMIR REFIT RTS and ITS will consequently enter into effect on the twentieth day following their publication in the Official Journal of the European Union, triggering an 18-month implementation period. The go-live date for EMIR REFIT is 29 April 2024.

+++

Since 2012, the European Market Infrastructure Regulation (EMIR) has been providing a uniform framework to make over-the-counter derivative transactions more secure and transparent. Since then, several smaller and larger changes have been made in a number of releases over the years.

The regulations that came into force in 2012 were expanded in 2014 and revised in 2017 in response to the experience gained in the first five years. This involved identifying issues and introducing potential improvements.

Now, the data and experience garnered so far is being used to bring EMIR up to spec. This is the job of REFIT, the Regulatory Fitness and Performance Program, which came into force on 17th June 2019.

Why REFIT?

The goal of EMIR-REFIT is essentially to improve data quality in reporting. The European Securities and Markets Authority ESMA has highlighted two significant areas here:[1]

- (Prompt) reporting of derivative transactions

- ESMA estimates that across all trade repositories, approximately seven percent of daily reports are submitted late. REGIS-TR calculates that approximately five percent of reports are submitted late, which translates as approximately one million reports per day.

- 3 to 3.7 million outstanding derivative transactions were not reported in 2020. According to REGIS-TR, this corresponds to about eight or nine percent of the total number of outstanding derivative transactions.

- The reconciliation process and the lower reconciliation rates

- 47 % of the reported, outstanding derivative transactions could not be allocated.

The goal is to encourage more reporting parity between companies.

What does REFIT mean for EMIR?

How is EMIR different in the UK and the EU?

Although the Financial Conduct Authority (FCA) aims to align the changes to UK-EMIR as closely as possible to the ESMA standards[2] and this approach is supported by industry associations[3], it is not yet clear to what extent it’s possible to harmonize EU and UK standards in line with the global CPMI-IOSCO reporting guidelines.

Even today, release dates sometimes diverge and it is questionable whether it will be possible for both systems to keep to the same timeline. This would involve maintaining two reporting workflows, and even small changes would result in a double workload for the developers. These uncertainties currently remain which means that the points above will carry a higher workload in all phases of a project.

What is the timeline for carrying out EMIR-REFIT?

On 10 June 2022, the Directorate-General for Financial Stability, Financial Services and Capital Markets Union (DG FISMA) issued a delegated regulation and an implementing regulation with appendix (see tables 1, 2 and figure 4, below) on the technical regulatory and implementation standards under EMIR-REFIT. These supplement the existing regulations. However, unfortunately, it did not include a specific timeline. These regulations will enter into force 20 days after publication in the European Official Journal.

What do non-financial counterparties have to do?

- Requirements for calculating the clearing threshold

- The new threshold calculation applies immediately upon EMIR-REFIT coming into force.

- The calculation result must be reported to ESMA and the relevant national authority.

- If a company decides not to perform a calculation or if the result is above the threshold, the company is subject to the clearing obligation and potentially collateral obligations.

- The calculation must be carried out every twelve months

- If the result shows that company remains on the same side of the threshold, there is no need to make a new report to EMSA or the relevant national authorities.

- Changes to the reporting obligation.

- Mandatory delegation for all OTC derivatives has applied from 18th June 2020.

- The reporting responsibility for OTC derivative transactions with a non-financial counterparty (NFC) passes to the financial counterparty (FC) if the non-financial counterparty is below the clearing threshold (NFC-). Non-financial counterparties that do not exceed the clearing threshold can therefore choose whether they want to remain responsible for reporting their OTC trades, or whether to assign reporting to the financial counterparty in agreement with the latter. ETD transactions, however, must still be reported by the NFC itself. A non-financial counterparty is itself subject to the reporting obligation if it exceeds the clearing threshold (NFC+). Due to the points above, you need to weigh up whether transferring responsibility to the FC makes sense, especially as coordinating with them also involves a not insignificant workload.

- After this regulation came into force, many NFC- decided to continue to self-report their OTC trades as the reporting route to the registry was already in place.

- Changes to the reconciliation process

- The reconciliation process needs improving. This will involve introducing several new fields to the reporting process.

- Improving and expanding the reconciliation process will be done in two waves.

- Tweaks to the reporting process

- REFIT is introducing a new action, revive, which will reactivate deleted contracts (see. figure 3).

- Current actions are still valid, but may have been clarified (see Table 1).

| Action | Definition |

| New | The first report of a derivative at trade or position level. |

| Modify | A change in terms or details pertaining to a previously reported derivative at trade or position level. This is not a corrected report. |

| Correct | A report correcting false information in a previously submitted report. |

| Terminate | Terminates an existing derivative at trade or position level. |

| Error | Cancels a duplicate report or an erroneously submitted full report if the derivative doesn’t materialise at trade or position level or is not subject to the reporting requirements in regulation (EU) No 648/2012 but was erroneously reported to a trade repository (TR). |

| Revive | Reactivates a derivative at trade or position level that has been either cancelled or accidently ended by the error action. |

| Valuation | An update on the valuation of a derivative at trade or position level |

| Margin update | An update to margin data (securities). |

| Position component | An update to a report on a new derivative contained in a separate position report from the same day |

Table 1: Types of action[5]

- As well as actions, REFIT is also introducing events (see Table 2).

- This makes it necessary to amend the status model in the reporting systems.

- Once terminated, a reporting cycle can now be reactivated. Current logic trees may need to be amended to accommodate this.

| Event | Definition |

| Step-in | An event in which part of a derivative in transferred to another counterparty (and registered as a new derivative) so that the current derivative is either terminated or receives a new nominal value. |

| PTRR | Risk reducing measures once transaction has been completed |

| Early termination | Terminating a derivative at trade or position level |

| Clearing | Clearing as per article 2 paragraph 3 of EU Nr. 648/2012 |

| Exercise | Counterparty partially or fully exercises an option or swaption |

| Allocation | An event in which an existing derivative is assigned to different counterparties and designated as new derivatives with reduced notional amounts. |

| Credit event | Applies only to credit derivatives. A credit event that results in a change to a derivative at trade or position level. |

| Inclusion in position | Including a CCP-cleared derivate or CfD in a position, whereby an existing derivative is terminated and either a new position is created or the notional value of an existing position is changed. |

| Corporate Event | An event in a company which has an impact on identifying the company and its derivatives (e.g. mergers & acquisitions). |

| Update | Update to a outstanding derivative during the transfer period to ensure it complies with the changes to reporting requirements. |

| Trade | Closing a derivative or renegotiating its terms, but with no change in counterparty. |

Table 2: Types of event[6]

- This results in new combinations at transaction and position level which need to be permitted and checked for plausibility by a reporting system (see Figure 4).

- Generating a Unique Trade Identifier (UTI)

- ESMA understands the importance of determining who is responsible for generating a UTI to prevent confusion. Figure 5 shows the decision tree used to identify who generates a UTI.

- This is a clear template to decide who is responsible for generating a UTI. However, it does not ensure that the UTIs generated are unambiguous.

- Changes to formats

- REFIT introduces the ISO 20022 format.

- REGIS-TR (RTR) has compared the ISO 20022 format to the current format used and considered the effects of changing (see Table 3).

| Proprietary RTR schemas | ISO20022 | Effects |

|

|

|

Table 3: Comparison of ISO 20022 and proprietary schemas and the effects of moving to ISO 20022[9]

- Changes to validation

- As can be seen from the timeline, concrete details on the validation rules will be given when ESMA announces the key information.

- Additional reporting information

- REFIT divides fields among three tables[10] à 203 fields including overlapping information in tables 1 & 3

- Table 1: 20 fields

- Table 2: 154 fields

- Table 3: 29 fields

- Fields are currently divided between two tables à 129 fields

- Table 1: 35 fields

- Table 2: 94 fields

- REGIS-TR, for example, differentiates between the additional reporting information as follows. (see Figure 6).

- REFIT divides fields among three tables[10] à 203 fields including overlapping information in tables 1 & 3

Conclusion

For many, reporting obligations are a necessary evil that entail extra work on top of day-to-day business. That the changes coming with REFIT promise to make things easier for the reporter is not apparent at first glance. REFIT seems to increase reporting complexity rather than decrease it. Many details are not yet clear and so often, the devil is in the detail.

REFIT will certainly increase data quality and transparency for the supervisory authorities. However, for the time being, EMIR-REFIT is an elusive concept as the RTS start date is further delayed and we are still waiting for concrete details on validation rules, reporting guidelines and process description by EMSA and the trade registers.

Furthermore, there is the risk that the EU’s and the UK’s demands on REFIT could diverge. Even though the FCA is aiming for as similar a variant as possible, this doesn’t mean that they will be keeping to the same schedule or that demands will be identical. This makes it all the more crucial to look at the current material as soon as possible and to determine the resources needed for a project to provide a reporting solution which is as standardized and automated as possible. One which makes it as easy as possible for an individual to use in their day-to-day business. Then, as written above, the reporting obligation would just be a necessary evil.

How can SEEBURGER help?

SEEBURGER’s Post Trading Services give you a central, comprehensive platform to fulfil all your post-trading process requirements. Whether through its Trade Reporting Solution (TRS) or its cloud-based RRM+ solution, SEEBURGER has been providing EMIR solutions since reporting started in February 2014.

Using SEEBURGER’s range of solutions for financial services, you can master even complex challenges such as the upcoming migration to ISO 20022. The SEEBURGER Payments Integration Hub enables payments in real time in ISO 20022 format as well as many other payment formats such as EDIFACT, SWIFT, ANSI X.12, ACH, NACHA, BAI, and BACS – complying at all times with the necessary regulations.

Technical Whitepaper

ISO 20022: Seize the Opportunity for a Modern Payments Integration Hub

[1] https://www.youtube.com/watch?v=Dykb3SpReRc

[2] https://www.fca.org.uk/publication/consultation/cp21-31.pdf

[3] ISDA-Response-to-UK-EMIR-Reporting-Consultation-Paper-021622.pdf

[4] Source: esma74-362-824 Final Report S. 48 DIAGRAM 1 ALLOWABLE SEQUENCIES OF ACTION TYPES – ESMA74-362-824 fr_on_the_ts_on_reporting_data_quality_data_access_and_registration_of_trs_under_emir_refit JOANNA (europa.eu)

[5] Source: esma74-362-824 Final Report S. 44 TABLE 2 PROPOSED ACTION TYPES – ESMA74-362-824 fr_on_the_ts_on_reporting_data_quality_data_access_and_registration_of_trs_under_emir_refit JOANNA (europa.eu)

[6] Source: esma74-362-824 Final Report S.44/45 TABLE 3 PROPOSED EVENT TYPES – ESMA74-362-824 fr_on_the_ts_on_reporting_data_quality_data_access_and_registration_of_trs_under_emir_refit JOANNA (europa.eu)

[7] Source: esma74-362-824 Final Report S. 45 TABLE 4 COMBINATIONS OF ACTION TYPES AND EVENT TYPES – ESMA74-362-824 fr_on_the_ts_on_reporting_data_quality_data_access_and_registration_of_trs_under_emir_refit JOANNA (europa.eu)

[8] Based on: REFIT Post Event Material – REGIS-TR – https://www.youtube.com/watch?v=Dykb3SpReRc

[9] REFIT post event material – REGIS-TR – https://www.youtube.com/watch?v=Dykb3SpReRc

[10] https://ec.europa.eu/transparency/documents-register/api/files/C(2022)3589_1/090166e5ed4b0167?rendition=false

[11] REFIT Post Event Material – REGIS-TR – https://www.youtube.com/watch?v=Dykb3SpReRc

Thank you for your message

We appreciate your interest in SEEBURGER

Get in contact with us:

Please enter details about your project in the message section so we can direct your inquiry to the right consultant.

Written by: Tobias Hevekerl

Tobias Hevekerl joined econtea GmbH in April 2016 and is a senior consultant, supporting utilities customers in project management, writing product requirement documents, running proofs of concept, optimising processes and product and test management. He advises the SEEBURGER product management team on the company‘s Trade Reporting Solution and RRM+. Following a traineeship in the commercial arm of an energy company and a degree in business informatics, from 2007 Tobias Hevekerl worked for two consultancies where he specialised in the utilities sector. In his free time, he likes to go hiking, jogging or cycling in the countryside. He also has a taste for adventure. He is a versatile sportsmen, enjoying mountain biking, climbing, zip lining, wall running, tackling high ropes courses, football and – unusually for a North German – skiing and snowboarding.