EBAday 2020 – The Payments Event for Financial Institutions in Europe

| | Senior Business Development Manager, SEEBURGER

EBAday 2020, a virtual event that took place 24 – 26 November, is the European Banking Association’s (EBAs) event for the financial industry focused on payments. This was the 15th EBAday, but the first to be completely virtual. Session topics covered Open Banking, digital payments, real-time payments, anti-money laundering (AML), request-to-pay, ISO 20022 and more.

Here are some useful highlights from EBAday 2020, in case you weren’t able to attend.

Open Banking

The speakers in the session “How open is Open Banking?” discussed their own banks, including J.P. Morgan, ABN AMRO and NatWest, and brought practical information about where this trend is now and where it’s likely to go. Today, banks are often opening one step at a time, at first using APIs internally, then moving to commercial APIs and creating an ecosystem with the goal of creating better services and improving the customer experience.

Speakers also addressed the question, “Do customers accept giving account access to third parties?” but, it appears trust is just one issue to tackle. Banks also need to be attractive partners for others, such as lenders, Fintechs and other banks for collaboration.

All of this takes investment and time, along with trust that APIs are safe and secure.

For corporate banking, APIs can be used to integrate with existing rails. Real-time data can be used for instant payments. One speaker admitted that they need further automation, easier integration and digital onboarding, along with an easier way to develop and expose APIs.

Real-time Payments

For the session “Instant, open, everywhere – have real-time payments delivered on their promise?” digital payments experts from different areas of the industry discussed the current status of real-time payments globally, and how banks can successfully navigate the remaining technological and operational challenges of real-time payments.

In developing or emerging economies, real-time payments are becoming critical (India 40%, Russia 42%, Mexico 29% real-time, for example). However, in the developed world, the comparison of real-time payments to total payments is low, e.g. Sweden 9%, NL 2%, Australia 4% (all based on CPMI 2019 data). A recent study by Ovum forecasts that instant payments will overtake EU-wide card usage by 2025.

According to one speaker, real-time payments drives the consolidation of all platforms. Banks need to decide what their role is in the digital payments process. Are payments a critical part of my business, or do I only support them?

So what are the benefits of real-time payments? Reduced cost is the main benefit, according to one speaker, and can be used to attract new customers. As far as progress with real-time payments among banks goes, the majority of large banks have achieved real-time payments, but most tier 2 banks are not real-time ready.

Reaping the Potential of Real-time Payments

In a survey conducted in this session about the benefits of real-time payments, 39% of attendees said they are currently building real-time propositions for their business customers, and 39% said they already have real-time propositions for their business customers. In the same survey, when asked what is most important to their business clients, 29.9% said richer data with payments is most important, and 25.4% said cross-border real-time payments was most important.

Euro Banking Association and McKinsey & Company on the Future of European Payments

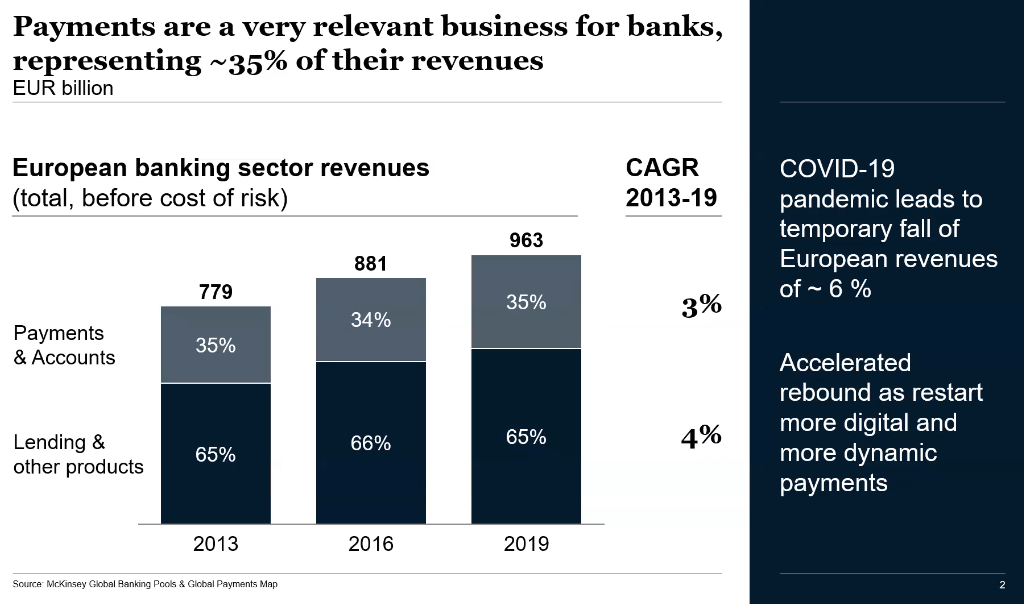

According to McKinsey, payments represent a good source of revenue.

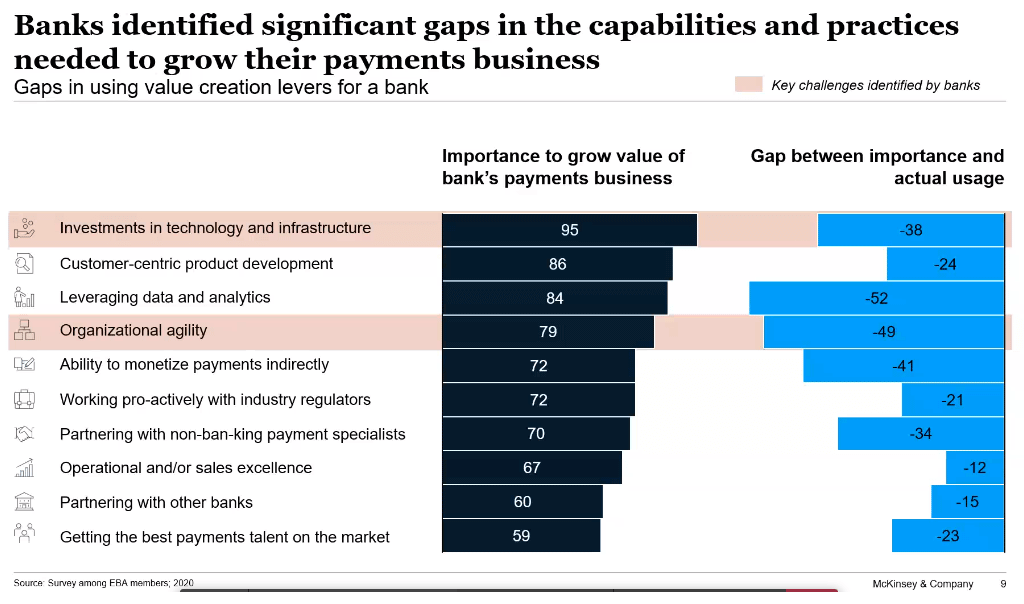

However, banks see gaps in the capabilities they need to grow their payments business.

In this session, McKinsey also stated that “Banks urgently need to develop a detailed plan for their future in payments.” Banks need to:

- Assess your starting point and spell out strategic ambition

- Define your payment business strategy and your key differentiating proposition

- Plan for strict and fast implementation of concrete actions

Highlights and Quotes

“The pandemic has served as a catalyst for digitalization across the entire industry. This has perhaps been the largest long-term impact, with the increased investment in and roll-out of virtual channels having played – and continuing to play – a critical role in helping banks and their employees keep the lights on. Deutsche Bank, for example, has seen an uptick in the use of its digital signature solution, as well as its innovative app-based solutions such as Autobahn and FX4Cash.” – Marc Recker, Head of Clearing Products, Institutional Cash Solutions, Deutsche Bank(1)

Survey respondents and interviewees identified a number of challenges faced by banks. These included increasing competition (especially from tech companies and Fintechs), the rise of technologies that could allow other payment providers to come between banks and their customer relationships, the lack of flexibility in banks’ operating models, the constrained revenue environment, rising customer expectations, and the complex regulatory outlook. Executives also identified gaps in the capabilities and practices needed to grow their payments business, especially in technology, organizational agility, and monetization models.(2)

Closing Roundtable

In general, banks feel they have made great progress in 2020, and partnerships have come into the spotlight. In 2021, key topics for banks will be continued digital transformation and customer journeys.

How SEEBURGER Helps

SEEBURGER helps financial institutions with payments modernization to prepare for real-time payments, Open Banking and more. With SEEBURGER you can handle all payment requirements, file formats and message types, automate and speed up digital payments, reduce risk, ensure compliance with regulations, create transparency and enable reconciliation. Our platform helps you to meet customer demand, simplify payment processing, increase automation and lays the foundation for ISO 20022 message compliance.

To discover more, download

“Financial Institutions: Modernize to meet customer expectations and gain market share.”

“Financial Institutions: Modernize to meet customer expectations and gain market share.”

(1) Business@EBAday2020, ebaday.com, November 20, 2020.

(2) “The future of European payments: Strategic choices for banks,” The Euro Banking Association (EBA) and McKinsey & Company, November 2020.

Thank you for your message

We appreciate your interest in SEEBURGER

Get in contact with us:

Please enter details about your project in the message section so we can direct your inquiry to the right consultant.

Written by: Matthew Burns

Matt Burns is Senior Business Development Manager at SEEBURGER, based out of SEEBURGER’s UK office. Matt has been active in the financial services market since 1991, having worked in a variety of roles ranging from EDI and EIPP to payments, cash management and Supply Chain Financing. He has worked extensively over the years in providing software solutions to global banks, multinational corporations and FinTechs, all with the common theme of improving business process, enhancing end-to-end data management and ultimately delivering an optimum experience for the end customer. Matt hails from Cheshire in North West England where he lives on a small holding with his Wife, two children, four horses, two goats, six chickens and two cats. He enjoys marathon running, mountain biking, skiing, scuba diving, camping and progressive rock music.