E-Invoicing with ABC analysis

| | PM (D-A-CH) automated processing of incoming invoices non-SAP systems, SEEBURGER

How to choose the right supplier.

Global e-invoicing is becoming increasingly complex due to many different national e-invoicing regulations. Nevertheless, it does not necessarily make sense to require every single supplier to participate in e-invoicing. The important thing is to identify those suppliers who achieve the greatest benefits (for both sides) by using e-invoicing with relatively few mutual resources. Many decision-makers apply the method of ABC analysis with the aim of maximising sales and profits. But did you know that ABC analysis can also be applied to e-invoicing? With ABC analysis the suitable candidates for the sensible use of e-invoicing can be clearly identified.

ABC-Analysis – Definition

The ABC analysis was described by H. Ford Dickie (General Electric Company) in 1951 in his article ‘ABC Inventory Analysis Shoots for Dollars, not Pennies’ (in: Factory Management and Maintenance, July, 1951, Vol. 109, pp. 92-94). Dickie referred to the work of Vilfredo Pareto and Max Otto Lorenz for the method. This use of the fundamentals explains the thematic relationship to the Pareto principle. To this day, entrepreneurs use ABC analysis to optimize processes and maximize sales and profits using scientific findings. According to Dickie, the following advantages result from the use of ABC Analysis:

- Optimization of the planning processes

- Reduction of administrative costs

- Increase in profits

The title of his publication indicates the aim of the analysis is to achieve large profits, not ‘pennies’.

The idea of the ABC analysis is to achieve a relatively large share of success with a relatively small input of resources, if you focus on the right place. Resources are not only of a financial or material nature, but also time in the form of effort plays an important role – because time is money. The ABC analysis shows where special commitment is worthwhile and where average efforts are sufficient.

Historic background of the ABC-analysis

The starting point for the considerations was the Pareto principle, which goes back to the Italian economist Vilfredo Pareto. He recognized at the beginning of the 19th century that in Italy 80% of assets belonged to 20% of the population and recommended at that time that banks should concentrate on this 20%.

The starting point for the considerations was the Pareto principle, which goes back to the Italian economist Vilfredo Pareto. He recognized at the beginning of the 19th century that in Italy 80% of assets belonged to 20% of the population and recommended at that time that banks should concentrate on this 20%.

The realization that a relatively small input of resources for the most important tasks contributes more to success than a high input for less important things can be transferred to many areas of business and life. The principle that in the right place 20% of the effort leads to 80% of success is a rule of thumb based on experience. These limits are by no means fixed, but are only guidelines. When applied to e-invoicing this can mean, for example, that suppliers are ranked by the number of their paper invoices in order to switch to e-invoicing (taking the top 20%). In this way, with the 20% of suppliers that have the most invoices in the ranking process, a total of 80% of invoices can be exchanged electronically using the Pareto principle.

ABC analysis – the refinement of the Pareto principle in supplier selection for e-invoicing

The ABC analysis was derived from the Pareto principle or the 80/20 rule, according to which only 20% of suppliers are responsible for 80% of the total invoice volume. This results in a division into two classes: ‘suppliers with high importance’ and ‘suppliers with low importance’. The ABC analysis however, uses 3 classes:

Class A with approximately 80% of the total number of all invoices and classes B and C. If necessary, the procedure can be extended to any number of classes whenever this appears necessary and useful.

Class A with approximately 80% of the total number of all invoices and classes B and C. If necessary, the procedure can be extended to any number of classes whenever this appears necessary and useful.

The ABC analysis is very easy to apply to supplier selection in e-invoicing. The main advantage is the possibility of presenting results graphically and clearly. After the classification into ‘important’ (group A), ‘less important’ (group B) and ‘unimportant’ (group C), strategically important decisions for e-invoicing can be justified more soundly.

The division into three clear groups allows the ‘essential’ to be separated from the ‘insignificant’. After classifying the data into the three groups mentioned above, an overview of the current situation can be created and strategically relevant recommendations for action can be derived from it.

Implement ABC analysis for e-invoicing in six steps

Which invoice exchange channels are suitable for which suppliers?

Due to relatively high technical requirements and costs in the exchange of electronic invoices, such as EDI e-invoices or XML-based invoices in Peppol BIS 3 format, this form of invoice exchange is only worthwhile for a few strategic suppliers. These are characterised by the fact that, measured against the total number of invoices, they send relatively large numbers of invoices and often already use e-invoicing with other business partners.

The ABC analysis can help to quickly identify the strategic suppliers for e-invoicing. The following six steps show how the ABC analysis can be used to specifically address the individual invoice receipt channels of the vendors.

The implementation of e-invoicing with ABC analysis in the six steps mentioned above is explained in more detail below.

Implement e-invoicing in six steps with the ABC analysis

Step 1 – Definition of objects to be classified and their valuation parameters

The objects to be classified are listed in a table with their valuation factor. In this step, a table with vendor number and number of invoices p.a. is created.

Step 2 – Sorting the objects to be classified according to the valuation factor

From the ERP or accounting system, the number of invoices p. a. per supplier is exported and sorted in descending order by number of invoices.

Step 3 – Calculation of the relative proportion of annual invoices for each object

The relative share of the number of invoices p. a. is calculated in relation to the total volume.

Step 4 – Accumulation of relative shares from top to bottom

Starting from the top, the relative shares are cumulated.

Step 5 – Definition of class boundaries based on cumulative relative shares

ABC analysis does not prescribe rules for defining the boundaries between the three classes. This depends mainly on the decision the ABC analysis should support.

Examples of how to use ABC analysis to implement e-invoicing with suppliers:

- If the aim is to give special exclusive treatment to only a few important suppliers, the A-class may only include a correspondingly small proportion.

- If the support is to be reduced for suppliers who contribute only a small proportion to the success of the project, the threshold between B and C classes is set accordingly.

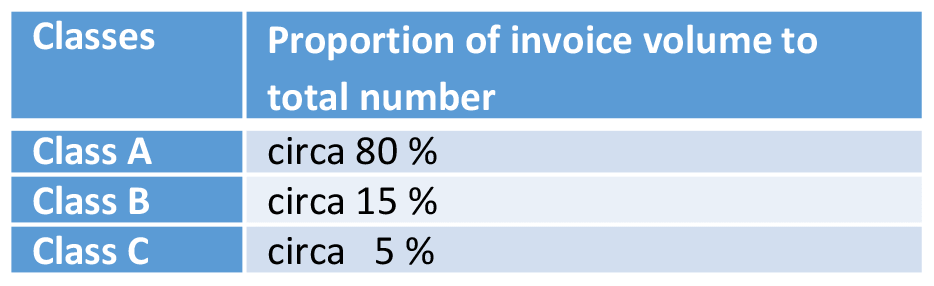

In an ABC analysis, it is common for the B class to comprise about 10 – 40 %, but this is not a fixed rule. In this example, for the onboarding of e-invoicing suppliers for the A-class 80%, B-class 15% and C-class 5% were selected.

Step 6 – Onboarding of strategic suppliers

For the high proportion of suppliers, who send a relatively small proportion of all invoices, the exchange of invoices via e-invoicing will tend to be unprofitable. This is why invoices are therefore mainly exchanged with these suppliers in PDF format or on paper. However, paper is the least economical and least ecological form of invoice exchange. In order to reduce the proportion of paper invoices to the total number of invoices, the possibility of exchanging PDF invoices via e-mail are particularly suitable for many non-strategic suppliers. SEEBURGER offers solutions not only for the invoice recipient, but also for the invoice sender, allowing savings of several euros per invoice compared to paper invoices.

Category A suppliers

Should be addressed immediately, by direct contact, e.g. via procurement, in order to convert them to e-invoicing.

Category B suppliers

Should at least be converted to PDF e-mail invoices in order to eliminate paper handling by the customer (invoice recipient).

Category C suppliers

Should not necessarily be taken into account for electrification, as they represent only a small share of the total volume of bills. In this category the switch to e-invoicing would not be economically viable.

E-invoicing solutions from SEEBURGER

The SEEBURGER E-Invoicing Solution offers controlled processing of incoming and outgoing invoices and extensions for the necessary process integration with any ERP system. SEEBURGER is an experienced cloud partner that understands the different requirements of different countries within the EU and beyond, and fulfils them with a one-stop solution.

Thank you for your message

We appreciate your interest in SEEBURGER

Get in contact with us:

Please enter details about your project in the message section so we can direct your inquiry to the right consultant.

Written by: Peter Fels

Peter Fels is Product Manager D-A-CH (Germany, Austria, Swiss) at SEEBURGER for the automated processing of incoming invoices for all non-SAP systems. Mr. Fels has many years of experience regarding the conversion from paper to the electronic invoicing processes.